Major Retirement Catch-Up Contribution Changes For 2026: A Plain-English Explanation of SECURE 2.0 and Roth Plans

Watch out: There are new regulatory changes to “catch-up” retirement payments from your older employees. If you fall out of line, you could open your company to penalties from the IRS.

Fortunately, these rules only impact high-earning employees—those who are earning at least $150,000 per year.

But you’ll still need to pay attention, even if you don’t currently offer a Roth option for retirement.

We have everything you should know right here:

Understanding the SECURE 2.0 Roth Catch-Up Requirements

Here are some of the most common frequently asked questions when it comes to understanding the new SECURE 2.0 Roth catch-up requirements:

What’s Happening With Retirement Plans in SECURE 2.0?

Starting January 1, 2026, high-earning employees over the age of 50 will no longer be able to make pre-tax catch-up contributions. Instead, they’ll be forced to make those catch-up contributions as part of a Roth—meaning they’ll be taxed beforehand.

Who’s Impacted By The Change?

The new rules impact individuals over the age of 50 who’ve earned more than $150,000 in Box 3 of their W-2s in the previous year with their current employer.

These high-earners are split into two categories:

- Regular Catch-Ups (Ages 50-59) – Maxed at $8,000 per year, as of 2026*

- Super Catch-Ups (Ages 60-63) – Maxed at $11,250 per year, as of 2026*

*The new rules say annual catch-up limits will increase with inflation each year.

Who’s Not Impacted By the SECURE 2.0 Change?

Those who aren’t impacted by the new rule changes include:

- Individuals who’ve earned less than $150,000 from their employer in the previous year.

- Individuals who are self-employed—even if they earn more than $150,000 per year.

- Employees who are in their first year with a new employer.

What Should You Do, As An Employer?

If you don’t have a Roth option in your 401(k), 403(b), or 457(b), consider adding one now—otherwise you may unintentionally penalize your older employees and make saving for retirement even more difficult.

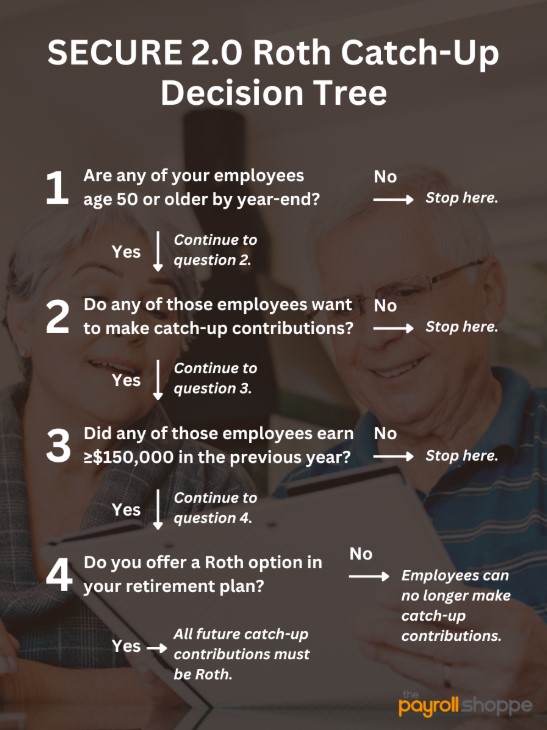

Your SECURE 2.0 Roth Catch-Up Decision Tree

If you’re still unsure how the new rules impact your company, follow our handy decision tree:

Question 1: Are any of your employees age 50 or older by year-end?

No – Stop here. No further action is required.

Yes – Continue to Question 2.

Question 2: Do any of those employees age 50+ want to make catch-up contributions?

No – Stop here. No further action is required.

Yes – Continue to Question 3.

Question 3: Did any of those employees earn at least $150,000 in the previous year?

No – Stop here. No further action is required.

Yes – Continue to Question 4.

Question 4: Do you offer a Roth option in your retirement plan?

No – Your employees can no longer make any catch-up contributions.

Yes – All future catch-up contributions must be Roth.

Find Support With Your Retirement Benefits

For additional help navigating the SECURE 2.0 rule changes, contact us.

Our Retirement Services are built to give you the resources, flexibility, and administrative support to comply with the updates while delivering a greater overall payroll experience to your employees.